Principle 3 of 8 reviews the criticalness of our collective ingenuity and collaboration in today’s business climate.

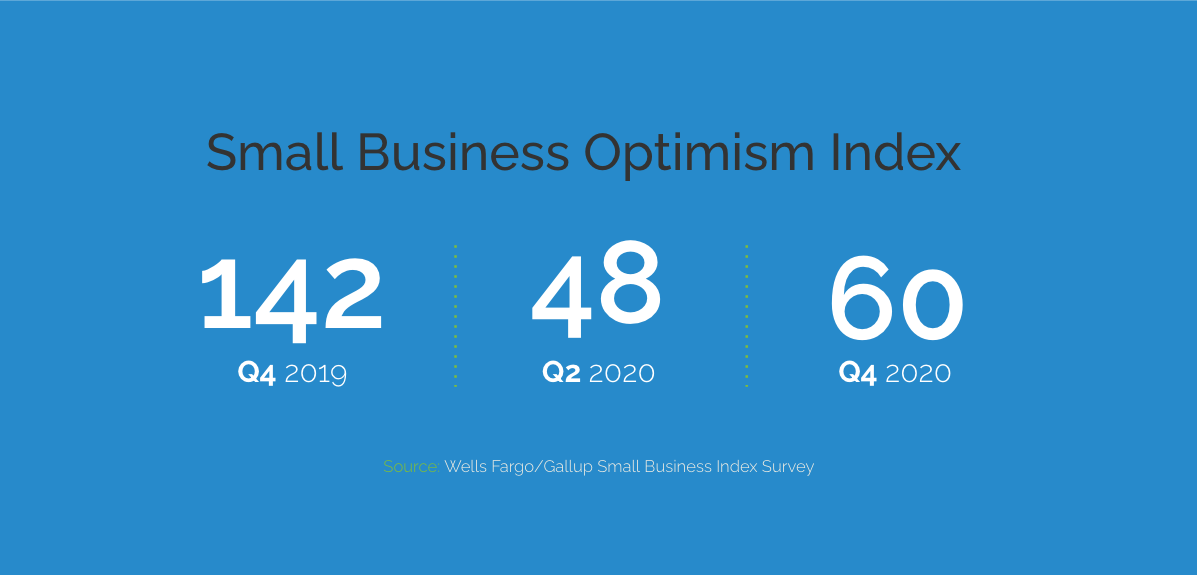

Unless you’ve been living in a deep hole since December of 2019, you’re aware of the increase in unpredictable challenges facing the owners of small businesses. Although the impact of the global pandemic on local businesses in the U.S. is too early to calculate in totality, the here-and-now struggle is vast and evident as SMBs focus on meeting safety guidelines for employees and customers, being inventive with operations and obsessing over cash flow. American grit is on display.

The rapid updating of health safeguards and testing of operational solutions vary by business size, sector and location. However, having a nimble financing partner—in combination with an existing bank relationship or not—is a growing necessity.

“Cash flow, even in a good economy is often a struggle for small businesses. But, now it has turned into one of the most, if not the most, important obstacle that they face.”

–Holly Wade | Director of Research and Policy Analysis,

National Federation of Independent Business (NFIB)

Ask yourself, “Is my financing partner limited to standard financing options that don’t fit my current situation, or are they able to work quickly outside those highly-regulated credit and loan products to create a customized financing solution for my business? If I’m doing everything in my power to keep my business open, am I alone or are there financing experts out there willing to match my effort?” In other words, do you have access to a short-term solution that builds a foundation for the long-term financial health and growth of your business? In other more-candid words, do you have a partner who geeks out on creative solutions for SMB financing? You’re not alone if the answer is “no.”

In her interview with CNBC Make It, Holly Wade of the NFIB stated, “Small business owners are having to navigate a very, very uncertain future right now and it’s not a one-size-fits-all impact on small firms. It depends on the industry, where they’re located, what the degree of the impact is on them.”

Small businesses have felt the cash crunch for decades as the bulk of institutional lending products gravitate toward financial requirements favoring mid-to-large size companies. In the small-business ecosystem, for example, success doesn’t guarantee growth because a small business is powerless against a bigger company that can dictate longer terms for payment. Or for businesses with seasonal revenue, no matter how predictable, opportunities have to be timed perfectly or they are nothing more than lost opportunities. Layer on the unexpected challenges, such as the current pandemic, and you’re wading through a perfectly ugly storm.

So How Best To Navigate the Current Environment?

Finding your way through the maze of barriers will take a new perspective on your core business, back-up plans for your back-up plans, and a look beyond traditional lending options.

- Diversify. The duration and depth of impact from the pandemic is still unknown, so ‘waiting it out’ could mean waiting too long to act. A September report on the effects of Covid-19 on U.S. small businesses by the National Bureau of Economic Research (NBER) found that more than 52% of businesses responded to the crisis by providing online services, 35% expanded digital payments, nearly 26% used delivery services, and about 25% used curbside pickup. On the other hand, 36% of firms found it difficult to change the delivery of goods or services in response to the pandemic.

Whether you’re selling a product or providing a service, look at every possible way to use your equipment, facility, space, or equity to build or deliver something now in demand by your existing customer base or an entirely new customer base. - Add supplementary links to your supply chain. Plan ahead for circumventing slow production at manufacturing plants, scarce raw materials and the resulting price hikes. In July, a MetLife and U.S. Chamber of Commerce Small Business Coronavirus Impact Poll found that the most common action (32%) by respondents in preparing for a second wave was purchasing additional supplies or products to prevent a future shortage. No surprise business acumen here: If you can still sell what you’re making, make sure you can still make it.

- Find more financing. The NBER’s Covid-19 impact report is revealing here, as well, finding that only a quarter of small businesses had access to formal sources of financing through a loan or line of credit from a financial institution, and most businesses were reliant on personal savings and informal sources of financing. The biggest challenge (39%) reported by businesses? Access to capital.

Get familiar with the terms used by alternative lenders to describe the lending solutions they most commonly provide. Be sure to ask about their maximum facility amounts, advance rates, and fees. There shouldn’t be anything to hide, and you’ll have a better understanding of how quickly you could have access to cash.

Ledgered Asset-Based Lending (or Ledgered ABL) is structured like a line of credit with borrowing capacity established by combining the value of liquid assets in your accounts receivable and inventory. Each receivable is tracked and monitored for its performance, creating a real-time record used to recalculate maximum draws during the life of the contract.

Invoice Financing (or accounts receivable financing or factoring) is a common way to access cash that your customers have yet to pay. Maybe the payment terms on invoices with a specific customer are stretched out to 60-90 days, or maybe you have multiple outstanding invoices across multiple customers, effectively tying up a substantial amount of revenue you’ve already earned. Invoice financing is a risk-free way to access that cash.

Another common solution is Invoicing Financing with Inventory financing added to improve overall borrowing capacity. Rather than combining the value of your liquid assets, this structure treats your accounts receivable assets and inventory assets separately.

Collective Ingenuity Saves the Day

The resourcefulness of American business owners has been tested before and will be tested again. At this moment in time, your willingness to adjust, engage, collaborate, and dare to endeavor will have great influence on your business and its outcome.

If you haven’t already, surround yourself with family, friends, employees and partners who support your passion, your expertise, and grasp the importance of quick, nimble decisions. With this foundation, your ability to find the best solutions for your business will increase exponentially.

We look forward to hearing your ideas and comments on LinkedIn.